Insight

How 2025 Private Equity Forecasts Missed the Mark and What Comes Next

Private equity entered 2025 with a familiar set of expectations: meaningful rate relief, a broad rebound in deal

Learn More

Q4 2025 delivered a striking paradox across mid-cap and regional banking: nearly every institution in our coverage universe posted earnings beats, margin expansion, and confident 2026 guidance. On paper, the sector has never looked healthier. Beneath the surface, however, a more unsettling picture is forming—one where record profitability may be masking a precarious complacency about the structural pressures bearing down on the industry.

We analyzed earnings releases, investor presentations, and management commentary from 18 mid-cap and regional banks. The results paint a picture of a sector caught between exuberance and existential risk. This article unpacks both sides of the ledger—and asks the questions that most earnings calls conspicuously avoided.

The aggregate story is undeniably strong. Net interest margins expanded across the board. Fee income hit records at multiple institutions. Efficiency ratios tightened. CET1 ratios remain comfortably above regulatory minimums, providing ample room for capital return and M&A.

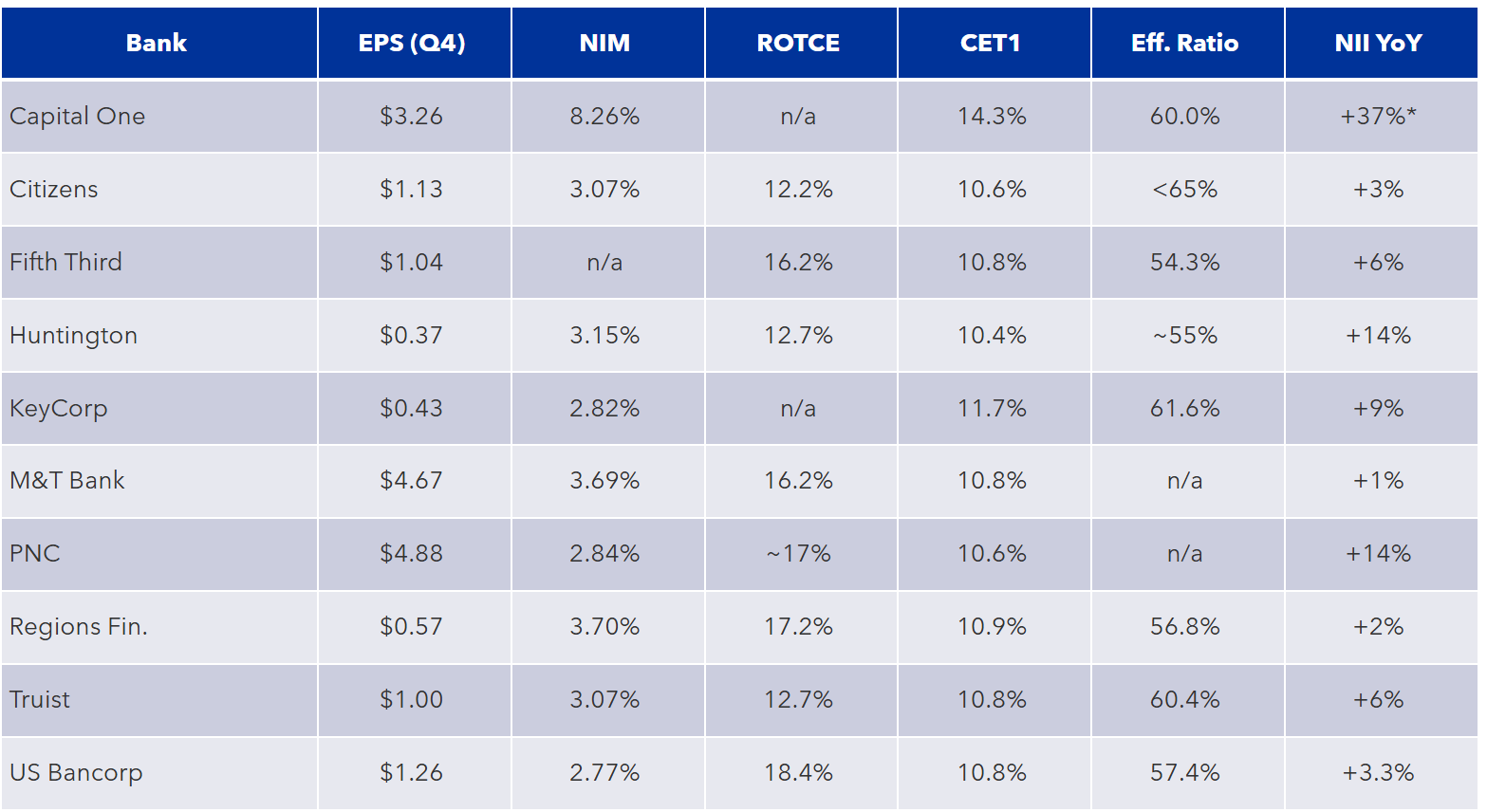

PNC led the pack among the large regional banks, posting strong fourth-quarter earnings that were up 25% from the previous year, driven by record revenue. M&T Bank closed out its best year ever with the highest earnings in the company’s history. US Bancorp continued to strengthen its profitability while improving its lending margins. Even banks that have been working through challenges showed strong momentum: Citizens Financial saw its quarterly earnings jump 36% compared to last year, while KeyCorp reported its highest annual revenue on record.

Exhibit 1: Large Regional Banks – Q4 2025 Performance Scorecard

* Capital One NII growth includes Discover acquisition impact.

Source: Company earnings releases, SSA & Company analysis

The smaller and specialty banks were just as impressive. East West Bancorp operated with remarkable efficiency, Western Alliance nearly doubled its income YoY, and Valley National continued its turnaround with improving profitability and lending margins that grew steadily throughout the quarter.

Exhibit 2: Smaller & Specialty Banks – Q4 2025 Performance Scorecard

Source: Company earnings releases, SSA & Company analysis

If Q4 earnings told one story, the M&A announcements told a louder one. Regional banking is consolidating at a pace not seen since the post-financial-crisis era—and the strategic logic has shifted decisively from defense to offense.

PNC’s $4.2 billion acquisition of FirstBank gives it access to Colorado and Arizona—two of the fastest-growing Metropolitan Statistical Areas in the country—and adds approximately $1 per share in accretive earnings by 2027. Fifth Third’s pending Comerica deal positions it to become the dominant commercial bank in the Upper Midwest. Huntington’s dual acquisitions of Veritex and Cadence are expected to produce revenue synergies well before cost takeouts are complete. And the Synovus-Pinnacle merger created a $117 billion combined entity overnight.

The message is clear: scale is no longer optional. Banks below $50 billion in assets that lack a credible path to $75–100 billion are increasingly vulnerable. The question is not whether they will be acquired, but when—and at what multiple.

Beneath the headline efficiency ratios lies an uncomfortable truth: technology spending is rising faster than most banks are willing to admit. Regions Financial disclosed that technology investment in its core modernization program will constrain M&A capacity until 2027. Banc of California is investing aggressively in back-end workflow technology, data optimization, and AI deployment. Western Alliance is planning to cross $100 billion in assets without a notable expense increase—an ambition that will test the limits of automation.

The banking industry is approaching a cost inflection point. Legacy technology architectures that once represented sunk costs are becoming active liabilities, requiring not simple incremental upgrades but wholesale replacement. Institutions that delay this reckoning will find themselves funding transformation at precisely the moment when margins compress—a scenario that rarely ends well.

The regulatory environment remains a source of acute uncertainty. Capital One’s 14.3% CET1 ratio reflects the buffer required to absorb the Discover integration, but it also signals the degree to which

regulatory expectations have ratcheted upward. The pending Basel III endgame rules, while delayed, continue to cast a long shadow over capital planning. For banks navigating simultaneous M&A integration and organic growth, the regulatory capital calculus has become a genuine strategic constraint.

Every bank in our coverage cited regulatory preparedness as a top priority—yet few could articulate the specific cost of compliance in their 2026 guidance.

Cybersecurity risk is understood by U.S. bank leadership, but it is often under-operationalized relative to the speed and scale of the threat environment. Survey evidence shows that cybersecurity is consistently ranked the top internal risk facing community and regional banks in nationwide surveys, with roughly 96% of community bankers describing it as “extremely” or “very” important.

While cybersecurity is widely identified as a top internal risk, it competes with external pressures such as net interest margin compression, funding costs, and deposit growth. In addition, only a minority of banks report their cybersecurity programs as highly effective, and many executives still see significant room for improvement in technology and IT maturity, suggesting a gap between investment intent and operational resilience. Industry research also indicates that most banks expect cyber threats to worsen in coming years even as they increase spending, reinforcing that the threat trajectory may be outpacing capability development.

In summary, the greater concern is not awareness but whether current governance, talent, and execution levels are sufficient to manage rapidly evolving threats, third-party dependencies, and AI-enabled attack vectors. Boards should therefore treat cybersecurity less as a compliance or IT issue and more as a core strategic and operational resilience risk requiring sustained oversight, benchmarking, and scenario-based stress testing.

Every CEO who spoke on Q4 earnings calls referenced talent as a strategic priority. Few offered concrete evidence of progress. The regional banking sector faces a compounding talent challenge: the executives who built these institutions are retiring, and the next generation of leaders increasingly views technology companies, private equity, and fintech as more attractive career destinations.

Huntington’s aggressive acquisition strategy is partly a talent play—buying relationship bankers and commercial lending teams that would take years to recruit organically. Western Alliance’s HOA banking and Digital Asset Group represent attempts to attract specialized talent through differentiated business lines. But the broader industry has yet to confront the reality that compensation structures, career paths, and organizational cultures designed for a pre-digital era are insufficient to attract the caliber of professionals needed to navigate the next decade.

Management guidance for 2026 was generally positive — and that itself should give sophisticated observers pause. PNC is guiding to 400 basis points of positive operating leverage. Huntington expects 10–13% NII growth. Valley National sees NIM expanding another 15–20 basis points. These are not modest expectations; they assume a benign credit cycle, stable rate environment, and continued economic expansion.

Exhibit 3: Selected 2026 Guidance – Key Growth Metrics

Source: Company earnings guidance, SSA & Company analysis

The risks to this consensus view are not trivial. Trade policy uncertainty—particularly the tariff implications that Western Alliance flagged for its manufacturing and technology clients—could disrupt loan demand in rate-sensitive sectors. Credit quality, while still benign (Zions reported a remarkable 5 basis points of annualized charge-offs), is showing early signs of normalization. And the yield curve’s trajectory remains hostage to a Federal Reserve that markets increasingly struggle to predict.

The institutions best positioned for 2026 share three characteristics: they have already made the capital investments in technology modernization, they possess differentiated fee income engines that reduce NII dependency, and they maintain the balance sheet flexibility to pursue opportunistic M&A. East West Bancorp, M&T Bank, and PNC Financial sit at the top of this hierarchy. Banks still debating their technology roadmap—or relying on NIM expansion alone to drive earnings growth—face a more precarious path.

Q4 2025 was a quarter of record numbers and record uncertainty. The mid-cap and regional banking sector has delivered precisely the kind of earnings performance that can breed complacency—and complacency, in an industry undergoing structural transformation, is the most dangerous posture of all.

The winners in 2026 and beyond will not be the banks with the highest NIMs or the most aggressive guidance. They will be the institutions with the intellectual honesty to acknowledge that record earnings are not a destination but a window—a finite period of strength from which to fund the transformation that the next decade demands. The question for every board and executive team in regional banking is the same: are you using this window, or merely enjoying the view?

Private equity entered 2025 with a familiar set of expectations: meaningful rate relief, a broad rebound in deal

Learn More

Excess inventory exists not because strategy is unclear, but because trade-offs are fragmented. A planner adds buffer to protect service. A plant batches to

Learn More

Matt Wilson shares perspectives with Supply Chain Management Review on how rising capital costs are intensifying the need

Learn More