Insight

Is Your Data Ready for the Era of AI-Powered Search?

Nick Kramer shares perspectives with Retail TouchPoints on how AI-powered search is reshaping retail discovery and why connected,

Learn More

For many years banks have been on a digital journey to improve service and efficiency, but success has wildly been varied – customer adoption hasn’t universally achieved the desired levels impacting cost efficiency.

Covid-19 has provided a shock to their system which changed the dynamic and made it clear that inertia was not an option. Digital adoption has rapidly increased at the expense of physical channels. As the CEO of a bank highlighted “Digital sales have increased to 75% of total sales from 25% earlier in the year, and they have achieved a shift in customer behavior which would have taken 10 years in 2 months.” Concurrently, the work environment has also dramatically changed– employees can and want to continue working remotely.

This presents banks with an opportunity to capitalize on these trends by accelerating digitization and cost reduction. Such transformation can be fast tracked, especially as leadership, having understood first-hand its benefits, will back initiatives to drive this change with far greater conviction.

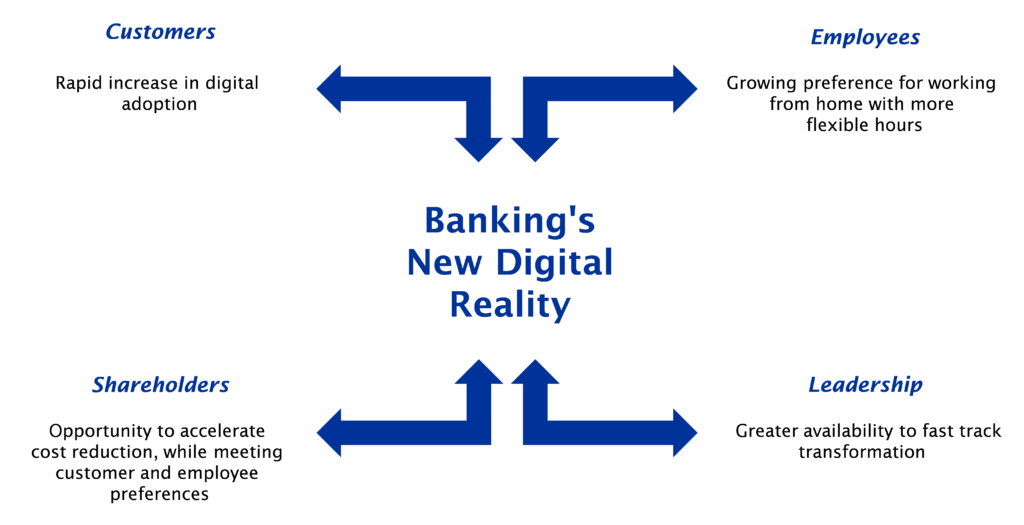

This is banking’s new digital reality. With all the stakeholders, i.e. customers, employees, shareholders, and leadership, all aligned around this mutual goal, banks have a window of opportunity to react rapidly and lock in this digital adoption, thereby avoiding reversion to the old world.

Customer and Employee Preferences have Changed

The current environment has shifted customers online for convenience and safety at a faster pace than ever with greater than 27% more likely to use digital channels.

The current work environment has forced the pivot of traditional office and call center roles into work from home positions, resulting in several positive developments. The technology has been stress-tested, and employees have enjoyed the work from home experience. Indeed, 66% of these employees would prefer to carry on working more remotely. Likewise, 70% of employees who have been permitted more flexible hours during Covid-19 would like to continue working in this manner.

From an employer perspective, this environment has resulted in a more flexible, engaged workforce that can provide extra availability to customers and management alike for specialist as well as routine activities. In addition, Banks can now access new talent pools leading to a more skilled workforce.

Now is the Time to React and Lock in These Changes in this Window

Banks need to embrace the customer and employee changes to make this an inflection point for the new digital reality. There are four key priorities for banks:

It is critical for banks to react rapidly in this window to lock in this change now.

Driving Remote Transformation Takes Discipline

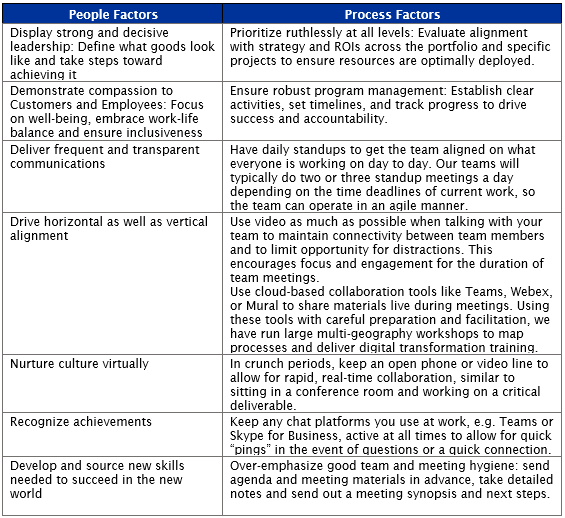

Delivering transformation under normal circumstances is hard. In today’s remote environment, that difficulty is amplified. In our experience of driving both large scale global transformation and smaller changes in this environment, success requires a calculated approach that considers both people and process – higher focus on people dimensions; robust discipline across the process of change delivery, supplemented with collaborative technology. Being flexible and adapting quickly is key.

The companies who will succeed are those who are rapidly embracing the change in customer and employee behavior, exercising discipline, and building operating models with agility and flexibility. These leaders are already working on what they need to do to improve their outcomes, and with it, grow market share.

SSA & Company can Help

Digital adoption has been a growing trend across financial services. The current environment has turbocharged this trend, and customers are now 27% more likely to use mobile, 28% more likely to use online, and 37% less likely to use a branch. Banks must use this as a catalyst to accelerate digitization and lock in this increase in digital adoption. SSA & Company is helping Financial Services companies re-invent, re-focus, and re-energize their businesses in these challenging times, driving transformation efficiently and effectively remotely.

Let us help you accelerate your digital transformation. You can learn more about our work in Financial Services here.

Customer research provided by Consumer Intelligence: Sample = 1,045, May 2020

Nick Kramer shares perspectives with Retail TouchPoints on how AI-powered search is reshaping retail discovery and why connected,

Learn More

Nick Kramer and Brian Nordyke share perspectives on why many insurance carriers are failing to realize measurable returns

Learn More

Nick Kramer shares perspectives on the governance, accountability, and operational risks organizations must address as generative AI adoption

Learn More